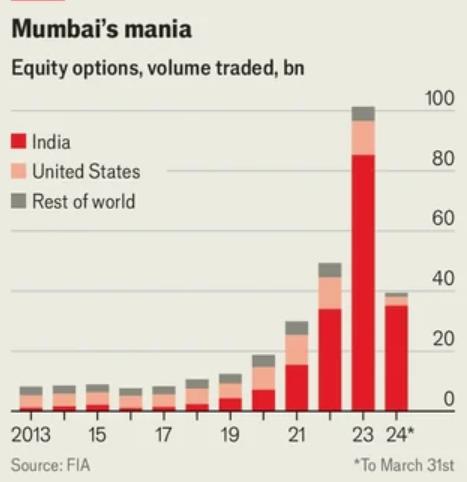

India’s options market has become the largest in the world by contract volume, but the foundation is cracking. In 2024, Indian exchanges accounted for 84% of all equity option contracts traded globally. That figure was just 15% a decade ago. The growth has been relentless. Monthly turnover in August 2024 hit ₹10,923 trillion. That’s higher than any other country. But the volume surge has come with a cost.

Retail traders are driving the boom. According to SEBI’s July 2025 study, 91% of individual traders in the equity derivatives segment posted net losses in FY25. That’s unchanged from FY24. Losses totaled ₹1.06 trillion, up 41% year over year. The average per-person loss was ₹1.10 lakh. The number of active retail traders dropped from 6.1 million in Q1 to 4.2 million in Q4. The churn is real.

The rise of 0DTE contracts is a major factor. These zero-day-to-expiry options are cheap, fast, and brutal. Most retail traders hold them for less than 30 minutes. They’re betting on intraday swings with limited capital and no margin for error. SEBI data shows over 40% of derivatives traders are under 30. More than 75% earn less than ₹500,000 annually. That’s a fragile base for leveraged speculation.

Hedge funds are feasting. Jane Street booked ₹36,700 crore in gains over 26 months before SEBI barred them from the Indian market. Proprietary firms are running high-frequency strategies against retail flow. The imbalance is structural. Retail trades are often momentum-driven, sourced from Telegram groups and social media influencers. The institutions are running models.

SEBI has responded. New rules kicked in between November 2024 and April 2025. Weekly expiries were restricted. Minimum contract sizes were raised. Premiums must be paid upfront. Intraday position limits are now monitored. The regulator is trying to slow the frenzy. But the volume remains high. Compared to two years ago, index options turnover is still up 14% in premium terms and 42% in notional terms.

India’s options market is now a story of scale and exposure. The liquidity is unmatched. The access is wide open. But the losses are concentrated. The market is being driven by youth, leverage, and speed. That’s not a stable mix.

Sources:

https://www.fia.org/marketvoice/articles/premium-turnover-indian-options-hits-150-billion